Consumer Psychology x Finance—Lessons from Social Sciences

- Thoughts

REBEL BLOG

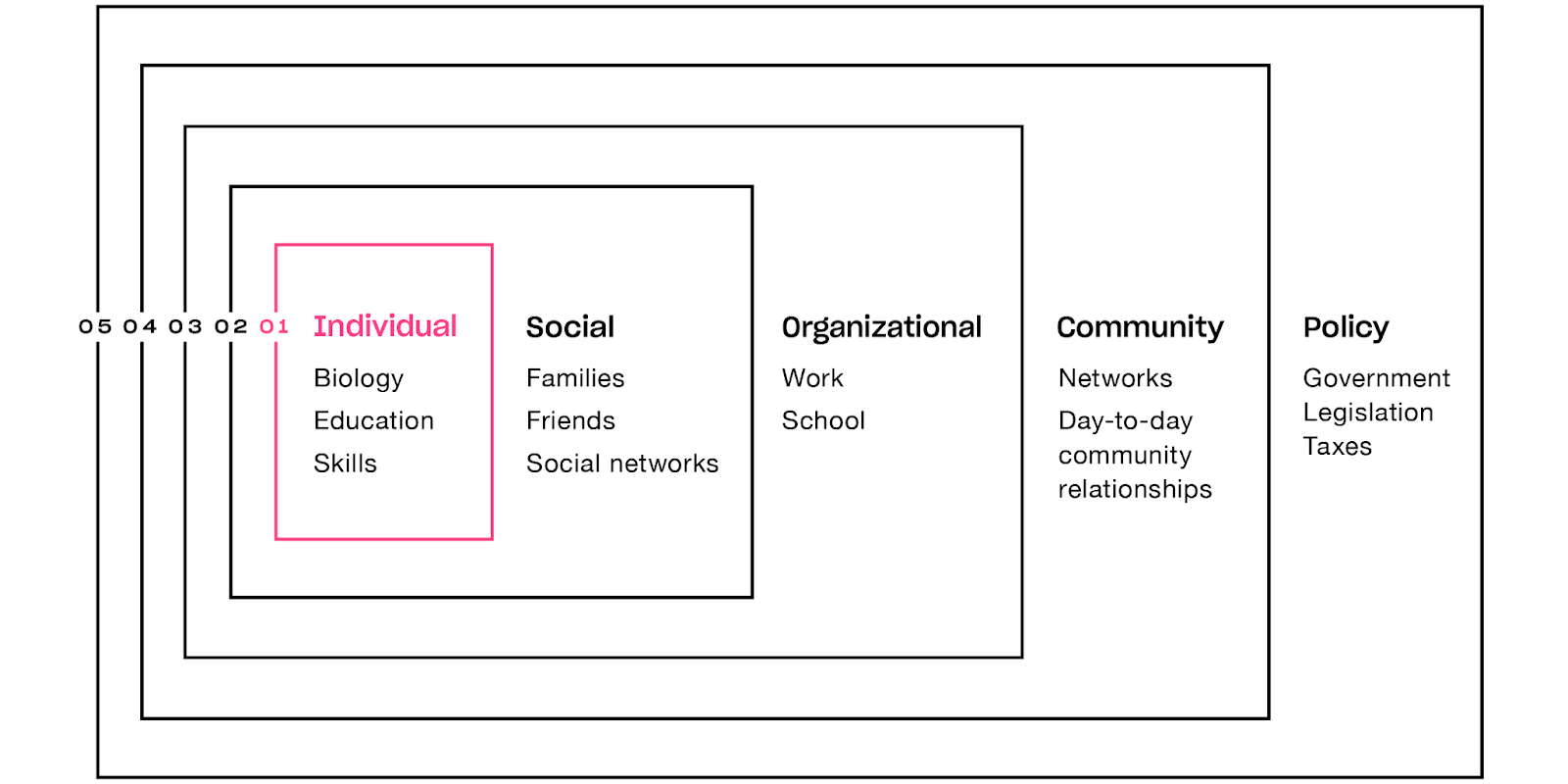

If you’re just joining us, we’re talking about how the social-ecological model can be applied to money behavior—and how finance brands can apply this idea. Here’s the link for the quick intro. If you’ve been following this convo, you’ll remember this little drawing I did on our proverbial whiteboard.

The first, most internal, layer of the ‘onion’—is the individual level. This level is specific to the person and is comprised of demographic factors such as age, race/ethnicity, or gender and acquired factors such as education, knowledge, income, or socio-economic realities. These factors originate with the person and are specific to that individual.

Our identities shape and inform how we exist and experience the world. For financial brands, understanding the nuances and behavioral complexities of audience segments can help shed light on how consumers are experiencing your brand and how best to serve them.

Age often marks important milestones met with decisions in one’s financial journey. The finance industry commonly uses these milestones to flag “when” an individual should be ready or a good fit for certain financial products or services. For example, once you hit 18 years old, you’re bombarded with credit card offers. OR—once you hit 50, you start receiving AARP retirement mail.

While no generation or age cohort is a monolith, age segments do provide context clues to global factors that often inform perceptions. For example, the oldest Gen Z’ers are entering their careers in the midst of high inflation, record-high college loan debt, and a competitive job market. Couple these factors with the fact that financial advice is casually available through social media and fintech is readily available—it makes sense that Gen Z brings nuanced expectations and banking needs to the conversation.

The nuance doesn’t stop with only age. Did you know that over 40% of Latino and Black individuals reported that they feel they need to change their appearance in order to interact properly with banks/financial institutions? Or, that women are more likely to attribute negative emotions (39%) (overwhelmed, out of control, and anxious) towards investing than men?

Moreover, beyond personal demographics, acquired influences such as education, financial literacy, and professional training can inform how we interact with money. For example, financial literacy, or how well one understands how to utilize and manage money, in general, is an indicator of better financial outcomes with spending, saving, borrowing, and investing. Rebel data has found this to be accurate as well—regardless of perceived (how well you think you are at financial literacy) or actual (how many questions you can get right about general finances) literacy—you are more likely to have better financial outcomes.

Reimagining segmentation to introduce behavior and contextual nuance can help make the money experience more human. Behavioral context can provide decision-makers with the insights needed to create real solutions that solve immediate and long-term pain points through service touchpoints, feature sets, or new products and offerings.

The financial industry is fast-evolving. Financial services' target audiences have never been more diverse or had more provider options. Approaching every segment as if it’s a monolith or trying to force a one-size-fits-all solution is not a real solution for today’s financial services. In fact, it’s the easiest way to disappear in the crowd.

Segmentation is not a new tool in marketing. However, by taking a more behavior-driven approach to segmentation— finance brands can create more human-centered money experiences and products. The result is brands and products that engender trust—which is desperately needed in the finance industry—and a stickiness factor that drives ongoing user engagement.

When brands, in any industry, understand the challenges, needs, pain points, and value propositions of their target customer—they are able to offer real solutions. And, when they offer real solutions, it’s easier to differentiate and continue to grow in an increasingly crowded market.

The financial industry is no different, the same rules apply here.

Get tons of industry research, useful data, downloadable templates, and more.