This model is traditionally seen through an academic psychology and public health lens. Public health experts use the model to create health intervention programming that empowers behavior change. For example, programs that work to prevent violence within communities, increase physical activity in communities, and smoking cessation have all leveraged the social-ecological model of behavior.

Although this model is most commonly utilized to create change in health behavior, there are no rules saying we can’t utilize these findings in other areas. Especially when the other areas are so deeply rooted in human behavior. Hint, hint—money.

Oh—and one other thing to make things more complicated. All of these influences also affect one another. Let me give an example—the community you grow up in (Level 04) can impact your education (Level 01). Or—The organizations you are a part of (Level 03) can also impact who you interact with regularly (Level 02).

The model is not an exact replica of the convoluted factors influencing behavior—but, rather, look at it as a cheat sheet for what to consider along the way.

The use case for finance.

Every one of our financial decisions is influenced by something. Sometimes, it’s an unconscious bias deeply rooted in our past experience with money. Perhaps the decision is based on what we know to be true about the circumstances we’re transacting. There are even moments when the decision depends on what we think we know about our future—and how this decision impacts that future. Either way, no one is making money decisions in a bubble.

Take, for example, a small decision like buying a morning coffee. It seems like an isolated decision—and for the most part—it’s a relatively benign decision. However, the decision to purchase a morning coffee is informed by a number of factors. For example, it can be influenced by your available budget (can you afford it?), your current circumstances (do you have enough time?), and your environment (perhaps the time of day, your next activity, the type of coffee you’re purchasing)—it’s not merely a simple calculation of 'to buy or not to buy' a cup of coffee. Even though it feels, in the moment, as if it’s just that simple.

Bigger ticket items—such as a car, a house, or a spendy vacation—all have different factors to consider, each with varying impact on the end decision. Moreover, decisions such as saving for retirement, investments, lending, or credit decisions can all compete with our inherent biases and past experiences with money.

For finance brands, it's important to consider the environment in which customers live and how it influences their financial decision-making. This understanding can create valuable experiences that drive adoption, foster long-term engagement, and ultimately improve outcomes.

The gameplan.

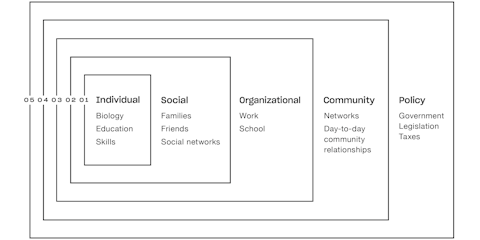

For this series, each article will focus on one of the five traditional layers of the onion (aka, the social-ecological model) as it relates to money behavior. We’ll talk about the key factors considered in each layer and how those factors impact or inform individual financial decisions.

- Level 01—Individual

- Level 02—Social

- Level 03—Organizational

- Level 04—Community

- Level 05—Policy

For our friends in the finance industry, we’ll provide context on what this layer means for ongoing engagement in financial products and services—and a few key recommendations on how to work with human behavior.

Let’s go.